It’s no secret that engagement rings are expensive. If you’re a traditionalist, expect to drop around two months’ worth of salary on a ring. If you’re not particularly traditional, it may still shock you to learn that the average cost of an engagement ring in the US is just under $6,000.

The cost of this important keepsake means that many grooms-to-be start looking at ways to finance an engagement ring. But while there are certainly a few options out there, it’s important to consider the implications of the repayment methods and whether or not you can realistically afford them.

So let’s take a look at some popular engagement ring financing options and what you should do to prepare for them.

Can You Finance an Engagement Ring?

Can You Finance an Engagement Ring?Yes, it is possible to finance an engagement ring. However, it’s important to approach financing with caution and ensure that you fully understand the terms and conditions, including interest rates and any potential fees. It’s advisable to only consider financing if you are confident in your ability to make the required payments within the agreed-upon timeframe. As with any financial decision, it’s crucial to assess your current financial situation and budget before committing to any form of financing.

Financing an engagement ring works the same as financing any other expensive item, such as a car or home remodeling. You get the money upfront to purchase the engagement ring then you are obligated to repay the money over a period of time or at a later date.

Whether you choose to use credit cards, personal loans, or a different method, you should (in most cases) expect to pay an amount of interest on top of the cost of the ring.

We’ve already established that engagement rings are not cheap. Deciding to finance an engagement ring may relieve the burden of the cost, but that doesn’t mean you should get carried away.

It’s tempting to get dazzled by those sparkling diamonds, and the desire to blow your loved one away with an amazing ring is strong. But before you decide how to pay for an engagement ring, you need to stop and consider a few things.

It’s likely that you have other regular financial commitments, such as a mortgage or rent, plus your monthly bills and other debt repayments. Don’t forget your usual monthly living costs on top of that, either.

The question you, therefore, need to ask yourself is, “can I afford another debt repayment?”

If the answer is a resounding “no,” then you must reconsider financing. No shiny rock plucked from the earth is worth getting into financial hardship over.

In this case, we’d recommend you save up and pay cash upfront. It may take longer, but you’ll be thankful you weren’t plunged into debt over a ring.

If you have room in your budget to manage another monthly financial outgoing, then the next question is, “how much?” No matter the amount, whether it’s $10 or $1,000, you must ensure that any repayment option you go for does not exceed it.

It is very common in the US to get an engagement ring financed. However, just because it’s common, it doesn’t mean it’s worth it.

If you plan to get engaged, then that means you plan to have a wedding. And weddings also cost money. A lot of money.

The average wedding in the US costs around $30,000. Add an expensive engagement ring into the mix, and you suddenly have a large amount of cash to find.

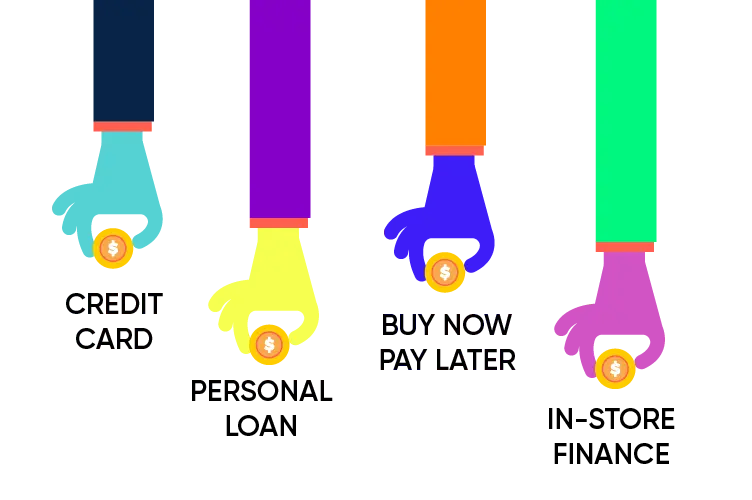

If you are determined to get financing for your partner’s ring. Here are some popular options to consider.

Using a credit card is the best way to finance an engagement ring because most of us have and use one already. Plus, it’s a quick and easy method that doesn’t require a lengthy application process.

Furthermore, if you feel your credit score is good enough, you could look into credit card issuers that offer an interest-free or low-interest promotional period.

You must, however, ensure you can make the minimum monthly payments otherwise, you’ll lose any promotional rate and potentially receive a fine.

A personal loan for an engagement ring can often offer more attractive interest rates than a credit card. Unsecured loans start at around 6% interest and have fixed monthly payments. However, to get the best rates on a loan, you will need to have a good credit score.

For engagement rings, Buy Now Pay Later loans are becoming an increasingly popular option among those with less than stellar credit scores, as this financing option only requires a “soft” credit check.

This option works by giving you the ring upfront in exchange for a deposit (typically around 25%). Then, you repay the remainder in equal payments over a short period.

Depending on the Buy Now Pay Later, engagement rings may or may not have interest added to the total amount. If you do, then you pay the deferred interest when your regular payments are due.

Most major online retailers have partnered with BNPL providers such as Klarna, Affirm, and Afterpay, and you will be offered this option at checkout, making it a very accessible financing option.

Two popular methods for in-store finance are store credit cards and jewelry store financing. They may even come with an interest-free repayment period when you first sign up.

You will be offered the financing at the point of purchase, but it is a good idea to research this option beforehand. You must beware that once the promotional rate on this type of finance is over, the interest can be very high and therefore become extremely expensive unless you pay it off fast.

It’s also worth noting that this financing method requires an excellent credit score so it isn’t for everyone.

Bad Credit ring financing is possible nowadays. The Buy Now Pay Later loan is available for those with bad credit scores as well as some jewelry stores that finance bad credit. However, if you have bad credit, question yourself as to why.

If you have a history of not making payments on time or defaulting on loans, is financing really the best option for you? Or is it just going to land you in more hot water? If so, consider saving and paying upfront for an engagement ring instead.

Not everyone that purchases an engagement ring upfront is rich. Many people are shrewd savers and have learned how to budget efficiently.

Our best advice is that the moment you feel like you’ve met the partner of your dreams, start putting some money aside, just in case. If things work out, then you’ll already have a cushion of cash to put toward the cost of a ring. If you and your partner split ways, then you can blow the cash on a great vacation!

Banks do can give an unsecured loan for engagement rings. The payment terms and interest rates vary depending on your credit score, so the better your score is, the better the terms you’ll receive.

FICO rates credit scores as follows:

To get approval for an engagement ring loan, you will need to be in the “good” category or higher.

Staunch traditionalists state that an engagement ring should cost two paychecks. Some even argue that it should cost three.

However, as the cost of living creeps ever higher, younger generations are ditching this idea in favor of much cheaper, non-traditional options such as lab-grown diamonds.

If you can’t afford an engagement ring, then it’s likely you can’t afford a wedding or financing, either. In this case, perhaps it’s sensible to wait to propose until you are in a better position financially.

Ultimately, you should only finance an engagement ring if you don’t have the money upfront and can comfortably manage the repayment terms. Weddings are a huge financial outlay, and while you want to make every aspect special, it’s never worth going bankrupt over.

If in doubt, have a frank discussion with your partner about a budget for a ring. There’s nothing wrong with finding a solution that works both for your wallet and your partner’s expectations.

Need help with more than just the engagement ring? We’re here to help!